fahd

fahd

There is a comprehensive article on Tradeciety that lists statistics from numerous studies and surveys about short term trading.

The article concludes:

After going over these 24 statistics it’s very obvious to tell why traders fail. More often than not trading decisions are not based on sound research or tested trading methods, but on emotions, the need for entertainment and the hope to make a million dollars in your underwear.

Rolf, Tradeciety

The stats that we found most relevant were these:

- 80% of all day traders quit within the first two years.

- Nearly 40% day trade for only one month before quitting. Within three years, only 13% continue to day trade. After five years, only 7% remain.

- The average solo investor underperforms a market index by 1.5% per year. Active traders underperform by 6.5% annually.

- Day traders with strong past performance go on to earn strong returns in the future. Though only about 1% of all day traders are able to predictably profit after fees.

- Traders with up to a 10 years negative track record continue to trade. This suggests that day traders continue to trade even when they receive a negative signal regarding their ability.

- Profitable day traders make up a small proportion of all traders – 1.6% in the average year.

- Traders tend to sell winning investments while holding on to their losing investments.

- Men trade more than women. And unmarried men trade more than married men.

- Poor, young men, who live in urban areas and belong to specific minority groups invest more in stocks with lottery-type features.

- Traders are more likely to repurchase a stock that they previously sold for a profit than one previously sold for a loss.

- Traders don’t learn about trading. “Trading to learn” is no more rational or profitable than playing roulette to learn for the individual investor.

- The average day trader loses money by a considerable margin after adjusting for transaction costs.

- Traders are overweight in stocks from the industry in which they are employed.

- Traders with a high-IQ tend to hold more mutual funds and larger number of stocks. Therefore, benefit more from diversification effects.

The above statistics were sourced from American and Asian demographics.

Australian statistics are similar

We wanted to see something more specific to Australia, and spent some time doing a review of existing material on short term traders vs long term investors.

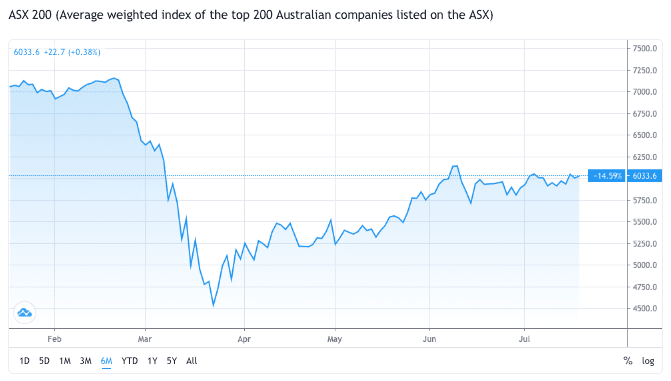

In general, the data shows that the average short-term trader in Australia underperformed the average investor by 6% per year.

A few years ago, that didn’t matter too much, as the Australian sharemarket had a long-term compound return of 12.5% per annum and retail investors / traders were averaging around 8% per annum. Institutions and corporate investors also used to outperform the index back then.

Currently, over 80% of active funds have not been able to beat the ASX 200 index in the last 5 years. We wrote about The three reasons Tabarruk beats the market, funds and short term trading in some detail too.

The trader’s delusion

Most traders I try and engage with about this, often remember their best trades and ‘forget’ their bad ones or don’t want to talk about those.

Most were also perfectly happy if they could generate 8% net return per annum. Even when I show them that by investing in an index fund that tracks the ASX 200 index, with next to no effort, they could’ve had a 12.5% return over the same period.

It didn’t matter to them that their trading costs, (plus other short term costs) and higher tax from selling shares in under 12 months, were higher. And that they underperformed a passive investment strategy.

They seem to have this delusion of doing very well, and proudly talk up their biggest wins, and underplaying or avoiding their losses.

I would push a bit at times and they admitted the losses they made in the past on stocks which had gone bust and they lost the lot – but these were no longer part of their current investment portfolio, so they tended to underestimate the cost of the duds.

I have a friend who is a professional investor / colleague from a past life. Anyway this friend tried short term trading with the shares of a company we hold at Tabarruk. It’s one of our major holdings and has done 300% in growth as of August 2020, with the upside potential some orders of magnitudes if the company continues on it’s current path.

Anyway, my friend bought and sold this company multiple times this year, holding a parcel throughout in his “investment portfolio” and chopping in and out with the rest, for small gains and losses in his “trading portfolio”.

When we compared our initial investments in this company, trading fees (brokerage) and our current net returns / growth, my growth was about a 100% more than his. His parcel that he initially bought and held outperformed his trading parcel by 200%.

This stark difference in numbers on the screens had him drop his jaw on the floor, followed by ‘And I spent hours watching the charts and trading this, which I will never get back’. I couldn’t resist a cooking analogy to drive my point home. Cooking a perfect steak means you don’t keep turning it!

Statistics generally show that well over 50% (and as high as 90%) of traders lose their money or significantly underperform, therefore we don’t try to beat those odds and we prefer invest long term with the Tabarruk Framework and Screening Process™. We do use pricing opportunities (often with alerts set in our broker platforms) to time our entry points.

Short-term trading is fraught with danger and often turns out to appear fairly random. For us, it is far easier to identify companies which are a long way below long term value and buy and hold them until they realise the inherent value, or until we can find something else with greater potential upside.

Misunderstanding between traders and investors

There is a basic problem here with short-term traders butting heads with long-term investors.

Some of the traders get up the noses of investors by implying they are smarties who are making profits on every twist and turn (highly unlikely when you consider the overall stats on trading) and some are trying to manipulate the situation by throwing around worrying comments, or by manipulating share prices directly.

Some of the investors seem to want the price to rise continually without any corrections and are worried that the traders will force an unjustified price fall.

We all know a continuous rise isn’t going to happen – and even if there are no traders out there, some get nervous and sell to “lock in profits” and some need to sell to fund their lifestyle – pushing the price down temporarily, even if it is worth much more in the future.

This arguing and misunderstanding has the aspects of culture wars – you’ll never convince the other side, so it’s better to work out your own investment philosophy and stick to it – don’t let others panic you into doing something against your own strategy and financial circumstances.

There’s no point people arguing with diametrically opposed points of view between trading and investing – you’ll never convince each other and it becomes philosophical and sometimes hysterical, with science and statistics ignored in favour of one-off “proofs” by someone who has a short term win concluding that just because they ‘won’ a short-term trade, they were right – very poor science, more arguing by anecdote and selective correlation.

Unsubstantiated comments like “the price has risen too fast” or “the market cap is unsustainably high” or “Company X will have to raise more money” can shock and unnerve investors – but there’s often no underlying science to them.

Our experience also shows the greatest potential upside in a share is the first decile of the price cycle when the the price starts to rise from an oversold “near death experience” i.e. when the price is ridiculously cheap but nobody has the guts to buy it and the last panic seller has just finished selling; and the second greatest potential is the tenth decile of the price cycle when everyone is piling in to a sure thing and pushing the price way above what I think it is worth – so don’t sell out too early!

And as always, this is not financial advice. Read our disclaimer.