Let’s compare two scenarios from recent research, done over the same timeline that demonstrates the real secret behind getting as close to possible in buying at the bottom and in effect, timing the market.

The results from the outcomes of both scenarios are quite interesting.

Let’s talk about TA. Technical Analysis, the world of pretty charts, graphs, and indicators. I break down why we don’t depend on them, and where they’re actually relevant.

Our journey into investment started as people who did a lot of technical analysis while buying stocks. I used to develop strategies with alerts set that triggered when technical indicators reached certain levels.

Over time we realised that technical indicators started losing their relevance in the current market settings. This is because these indicators were created when the market was a completely different machine, it came about in a time when trading was a retail business and trading was done on the floor.

Trading on the floor is a thing of the past

Suits with phones yelling across a floor, looking at screens with tickers and numbers are almost non-existent now, which is why our focus at tabarruk is on the companies themselves, analysing the fundamentals and the prices they trade at. Today, of the total volume of stocks being traded on the market, less than 15% of the volume comes from active fund managers and the rest comes from passive managers. The indicators lose their relevance due to fewer people actively trading to creating the effects of the indicator.

The other reason for not being overly reliant on technical indicators is that we live in an age, where things are automated. A lot of algorithms are created, even bots to trade the market, and this changes the whole landscape of the share market as it’s impossible to make a bot understand human language and emotions to describe something even we do not understand or comprehend.

A big driver in markets is sentiment. We’re yet to see bots or algorithms that can factor in sentiment correctly. We know of situations when an algorithm has reacted to a tweet or social media post, or a news bulletin and bough up stocks or sold them off and till today we still don’t actually know why.

My first mentor made it a point to drill technical analysis into my head and I learnt it well. But over time, what makes more sense to us is to watch for trends and realise that there is no way we can trade faster than a machine. This is why we do not call ourselves day trader, we don’t want to trade and we don’t want anything to do with short term trading.

Weekly & Monthly over Daily & Hourly

We spend more time looking at weekly and monthly charts than daily and hourly ones. Especially monthly charts because it gives us some powerful trend signals. What we’re trying to highlight here is that even though we don’t depend on technical analysis, it doesn’t mean we ignore the charts. This is because a picture paints a 1000 words, sometimes visuals clear up something better than a report. There are occasions when Moin likes to look at the interesting trends within a day to pinpoint an entry.

We often get asked if we are fundamental or technical investors. We’re neither. These were terms that were created for a market that existed in a different time. We use every resource and tool to help make a decisions in a time when hyperconnected-ness and events cause reactions in seconds.

Stock analysis is like a Biryani and there are so many different types of Biryani. There is Lucknowi, Kolkata biryani, Hyderabadi biryani and Srilankan Biriyani. Why would I limit myself to only one type of Biryani, it makes no sense.

I started investing seriously when I was 21. Even though I had some success, I kept making the same costly mistakes.

Forced to reflect

This made me reflect and come to a bitter conclusion that the success I experienced wasn’t mine to in the first place. It was because I followed my father’s advice. The disasters though, which taught me harsh lessons, were due to my hubris and bad habits.

I had the luxury of being someone who could make these costly mistakes and fall back in the safety net of a family that was supporting me through my university life, paying my fees and boarding. However, this was coming to an end and after a frank conversation with my Dad, who basically told me to pull my head in and that I had to change my habits.

We’re all creatures of habits and routines. Once set in our ways, we build a wall around our comfort zone and like staying within it to keep doing things the same old way. Initially unaware of my family paying the cost of the losses due to my bad habits, then being told to wake up by my father and being forced to look in the mirror was a very unpleasant experience.

I now realize the truth in the maxim that the catalyst any growth is one of two well-trodden paths. The first is change and the second is discomfort.

So what were the 3 habits that were holding me back and how did I get rid of them? Read on…

This is a topic that I wish was taught in schools, primary schools even. Like a lot of things, the earlier you start investing the better. I strongly suggest researching the benefits of compounding interest. This is where your money grows exponentially over time, due to time the money spends in the investment, not ‘interest’ interest as that’s something we want to avoid.

In this article, I am going to break down the 3 steps anyone can, but especially the young ones can use to start investing. I also share my story of how I learned to be a successful investor by breaking it down into 3 steps.

Step 1 – Learn, learn, learn

This may be a no brainer but you will be surprised how I had ZERO idea of how investing was done.

When I decided to make my money work for me, I was lucky I had my father, who mentored me and took the time to teach me the value of money and the rules of investment. It also helped that he was the Vice President of Treasury in Abu Dhabi Islamic Bank and the people I got to mingle with and ask questions to people who knew a lot about investing.

Step 2 – Pay off debts

The main rule my father imposed on me was that before starting to invest, you have to pay off your debts. There is no point investing if you have outstanding debts. This is because the way our current financial system is set up is to benefit the lender.

The longer you take to pay off a debt, the larger it grows. Interest makes the debt grow exponentially. Compound interest when used incorrectly, will work against you. Before you think of buying anything on the stock market, put that money towards your credit cards, personal loans or whatever form of debt you may have. They will hold you back long term.

Step 3 – Set aside a percentage

Next, think about your future and dedicate a percentage of your paycheque towards that. Rain or shine, you must automatically transfer 10-20% of your pay to this bucket. A separate account works best. This is where you will get the money to start your investing journey. No one becomes a millionaire overnight but every millionaire started with ZERO. Start your ZERO today.

In order to do this properly and decide how much you’re going to pay yourself, you need a budget. What this does is force you into limiting your spending. Sticking to a budget will help you get disciplined and decide how much you have that you can pay yourself with.

The more you pay yourself starting young, by giving up on the glitz and the glam, the better. I’m not suggesting avoid living altogether, rather make it work within your budget and not the other way around.

Your budget sets you up for success because the money you’re putting away can turn into hundreds of thousands of dollars. This is because your money can have the opportunity to work its compound magic over 20 to 30 years.

Bonus step – Write out a specific financial goal

Last but not the least, set yourself very specific financial goals.

Like, how much money you want to have invested by your 30s or 40s.

This will help you understand how much money you have to invest each year. Which in turn leads you to understand how much you have to invest each month. Which then helps you understand how much you need to pay yourself from each pay cheque and decides your budget.

Saving money costs you? How is that even possible you ask? Read on with an open mind to find out.

Saving money is important, but there is a difference between an emergency fund and saving money because we fear losing it.

Two rules someone who knew a little about investing said;

Rule 1: Do not lose money Rule 2: Do not forget Rule 1

Mr. W. Buffet

Paying yourself

If you’re an individual with a lot of savings, I have a lot of respect for you. That’s because you’ve understood the importance of paying yourself. A lot of people forget that when you get a payslip, it’s a reflection of your organisation paying you for your time.

From that payslip, how much do you pay yourself for your time and effort?

Regardless of what you’re earning, I think you should always set yourself a minimum of 10% from your pay to be put away as savings. This needs to be applied immediately if you want your financial vision to line up with reality.

Saving money is a very responsible thing to do, if you start this habit at a young age you generally end up in a good place financially. However, what will actually set you up for success is what you do with your savings! What you do with it decides how you live your life in the future. Whether you scrape by or live comfortably.

The invisible enemy

If the bulk of your money is going into a savings account, where you’re accumulating your cash, you’re actually losing an enormous sum of money in the long run. The reason you’re losing money is due to the invisible enemy.

No, not COVID-19 but the other deadly killer known as inflation. What is inflation? Put simply, inflation is the increase in prices of things and decrease in what your money can actually buy you. Ever heard your grandparents say how much bread, milk and eggs cost them in the past, and how ridiculous prices are today? Yup, that’s the invisible enemy.

Eggs as an analogy

Let’s compare $10 in the ’70s and $10 today in Melbourne. Let’s compare the purchasing power of a $10 note by looking at buying a dozen eggs.

In the ’70s a carton of 12 eggs cost $0.59 cents. $10 would buy you 16 cartons and you’d still have some change in hand.

Today, if you walked into Coles or Woolies, the same $10 will only buy you 2 cartons because a carton costs $4.70. That’s eggspensive!

This shows how the purchasing power of $10 reduced from 16 cartons to 2 cartons over the decades. This trend will continue into the future and we will be telling our grandkids how making eggs for breakfast today costs a fortune.

If that’s what inflation does to your eggs, imagine what it does to your savings.

Inflation & Interest

The annual rate of inflation is 3% per year. Therefore, it is shocking to see the average rate of interest for a typical savings account in Australia was only around 0.75% at the time of writing. This is more than three times less than the rate of inflation.

Effectively, we are faced with a unique situation where our savings, our hard-earned dollars, are losing their purchasing power and weakening as inflation eats away at it over time. As Muslims, this is amplified because we wouldn’t put money into interest-earning accounts!

You can probably wrap your head around the concept now. When you save money, over time it decreases in value and purchasing power. Wouldn’t you rather it work for you and increase in value? Despite knowing this as a concept, people continue to invest the traditional, interest-earning, safe-in-their eyes, way.

The fear of losing money

An important question to ask is, why do people rely on savings even if they know it to be an ineffective way to grow wealth?

The root cause is fear. People are afraid of losing money.

If you really think about it, not investing your money because you’re afraid of losing it is the same as saving your cash and losing its purchasing power due to inflation.

If you think you’re avoiding risk by saving your money, you will lose in the long run. I repeat, the lost opportunity that comes with saving money is the same as the money lost due to inflation. You are missing out on putting your money to work for you, by investing and growing your wealth.

What do you think the banks are doing with your savings anyway? They are investing it and saving the profit for themselves. The banking and lending industry did not become the behemoths they are today by equalising the playing field or helping the common person. They lend you peanuts and charge you an arm and a leg when they take it back.

Money invested makes money grow

Ever heard the phrase ‘You need money to make money’?

Let me expand that a little further; you need to spend money to make money.

If you use money to buy something, then sell that something for a profit, congrats, you just ‘made’ money make more money. Better than money sitting somewhere, not working, and deteriorating due to inflation.

This is the BIGGEST reason why investing in the stock market, regardless of its ups and downs, for the long term, gives you one of the best opportunities to grow your wealth.

Investing in the stock market, the Tabarruk way, helps your money make more money and benefit from the power of compounding.

Hopefully, you now agree with me, that saving money actually costs you.

How do you start saving and investing? Head over to our article, 3 steps to start investing? Generally speaking, I think people should focus on having a 3-6 months emergency fund in savings, and once you have put aside that, then enter the world of investing.

I’ll leave you with another quote from someone I should’ve listened to more often.

Before investing, learn how to save. If you don’t know how to save money you can’t learn how to invest it. Both these disciplines require discipline.

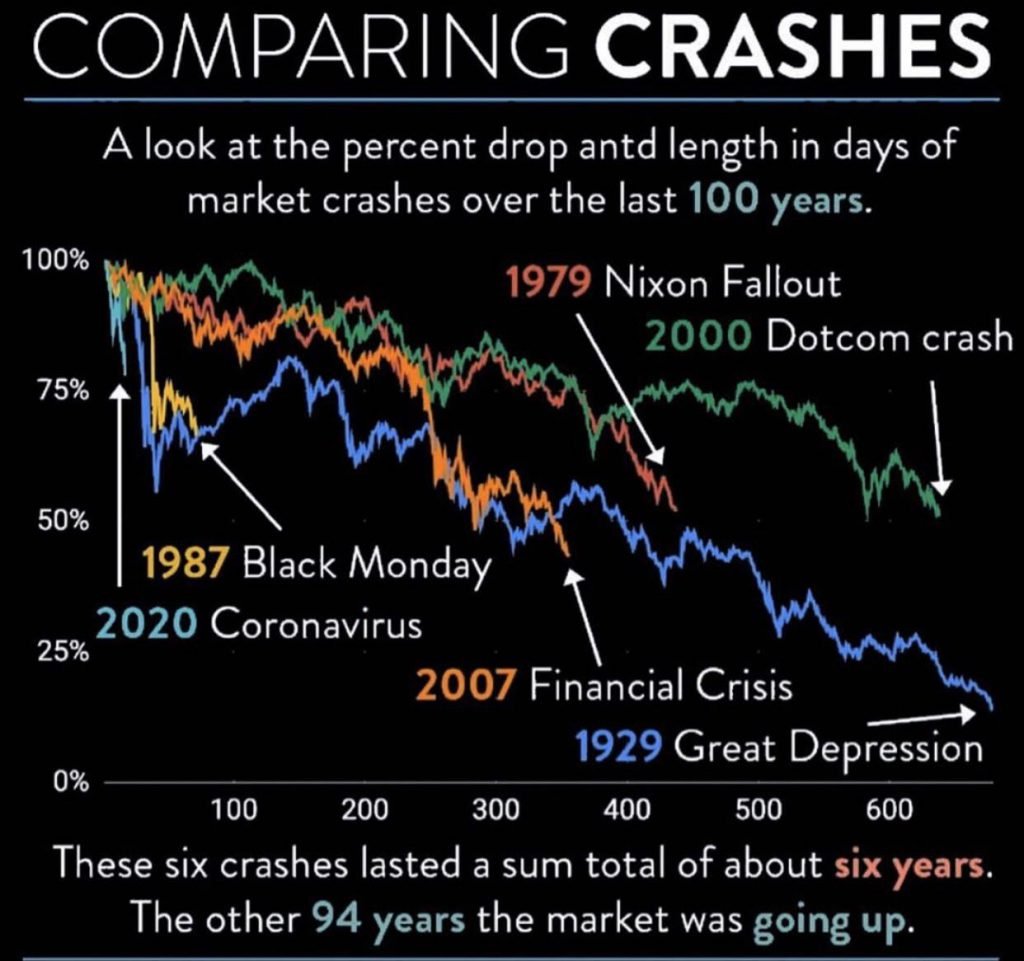

We ended Part 2 – GVC, Global Virus Crisis – Recovery on analysts drawing comparisons to past crashes. There is a lot to learn from the COVID Crisis, as the global economy was ground to a halt and unemployment jumped exponentially in an already fragile economic system.

Many analysts compare this collapse to the previous financial collapses the global economy experienced, however in this article I articulate what makes this collapse different and explore what options are available on the road to recovery.

Notable past crashes; there was the great depression in 1929, The 2001’s 9/11 attack caused market sentiments to plummet in the airline industry which in turn damaged the economy. Then the famous subprime mortgage crisis in the U.S that led to the great recession from which some countries still haven’t recovered.

Past crashes compared (only the downward phases)

It’s important to realise that even though history provides us with a lot of insights from past market crashes, even ones that experienced huge economic shocks and job losses, our current scenario is completely unique.

Speed of this crash

The current financial crisis hasn’t been created by a financial system that’s stretched to the limit. It’s caused by a pandemic which has occurred in a hyper-connected world, one that is much smaller than what our predecessors lived in. This combination of swiftness and magnitude of shock to the global economy is unprecedented.

In my view, the narrative being pushed by the media and a lot of analysts calling this a ‘financial crisis’, is just wrong. The globe is facing a health crisis and asking economists and financial analysts to fix the economy is going about it the wrong way.

The curve vs economy

The economy is, however, linked to the spread of the coronavirus. If proactive measures are not taken by the authorities to control the spread of the virus, the human costs will be severe and the ripple effect of this experience will have a negative impact on the economy due to loss of capability and efficiency.

Many countries around the world have come to understand this and there is a lot of focus on flattening the curve. This is how the crisis transformed from health into a financial crisis.

As countries around the world introduced lockdowns and enforced social distancing it has brought up an interesting conundrum.

Research has shown conclusively that the more aggressively governments around the world try to flatten the curve the deeper the worse the economic impact.

As the world continues to be in various stages of lock down, it is a foregone conclusion that we will experience an economic contraction.

However, to use the terms of recession and depression is not the most accurate. Right now the focus is on protecting people’s health, especially those most vulnerable and doing everything possible to ensure the health system doesn’t fold.

What cannot be denied is that the economic impact this causes around the globe is going to be painful and we do not need to look any further than people in the hospitality, tourism and travel industry. Overheads still remain and banks continue to charge interest on loan balances.

An eye on India and China

India is the best example of looking at the effects of COVID19. Their population of more than 1.2 billion is currently under lockdown. From this 1.2 billion, almost 500 million are unskilled workers who live mostly on a daily wage.

The ability of these people to keep their jobs hinges directly on the duration and extent of the lockdown. Essentially determining if they are able to put a meal on the table or not.

In the current times of instant gratification, it is critical to observe how the pandemic caused the supply and demand market continues to experience a tsunami of chaos. Supply has been derailed as borders, business and factories closed down which then affected demand as industries don’t need raw materials when they are not producing any finished goods.

There is not enough research on the global impact that the 25% decline in production from China will have on the global economy.

Prior to the pandemic, China was heading to a -1% projection on its GDP (Gross domestic product). This also does not take into account health care equilibrium. China exited theirs, only to find out the U.S. and Europe are knee-deep in theirs.

One country battling this health crisis successfully does not mean that international trade will return to normal. The supply and demand shock experienced globally can be witnessed by the chaotic rise and fall in global sharemarket indices.

Next steps

How do we come out of this crisis?

It’s simple! We first deal with the pandemic.

In the meantime, it is the responsibility of the government and central banks to keep the ship afloat and plug the holes.

Central banks around the world need to ensure that there is a steady supply of money flowing through the global financial systems. This is to ensure credit is available for individuals and businesses without cash or savings to bounce back.

Governments need to be smart and not deploy a parachute which only favours a few, like the last financial bailout. They need to invest money into a trickle-up economy, where the money is provided to those with lost earnings so they can maintain basic needs like rent/mortgage, utilities and meals.

Plan B

Leaders around the world need to have a discussion on a Plan B if the fiscal stimulus package does not have the desired outcome.

This is to ensure that countries that do not have the cash don’t inadvertently cause a domino effect which will drag the globe into depression instead of a recession.

Recession – An economic contraction when GDP declines for two consecutive quarters.

Depression – A severe recession with a 10% or more decline in GDP.

The United Nation has stated that the developing countries have lost more than $220 billion dollars and these economies will have the toughest time navigating this crisis. The gap between the poor and rich nations will increase which will lead to an exodus of financial refugees.

Even though the short term looks dire, the opportunities that have arisen from this crisis is massive. The first conclusion is countries need to invest more towards their health care system. If every country were to invest 3% of their defence budget towards their health care system, we can easily navigate another pandemic. A second wave or a future mutation, or a new virus.

Businesses are now thinking about the sustainability of the current financial system. How do we make it more resilient?

Wealth cannot buy health, and that’s why a truly resilient economy needs to have a resilient health system.

Health is directly related to our food production, what systems can be put in place to ensure our food production will not get hit.

The economic system that will emerge from the current crisis will be able to ensure that it can continue to go on feeding people and keep people healthy.

Health and wealth go hand in hand and hoarders never get far.

Unlike the last series of bailouts, especially here in Australia, where the governments are attaching strings to the money, they are providing businesses.

They want businesses to not eliminate their capacity and keep their employees on board for the next 6 – 12 months.

The Australian government has actually learned from the actions taken by the US and Europe in the last crisis. They understand it is very important that the money they provide the private sector goes into safeguarding individual incomes in the form of jobs.

In Australia and the West where we’re generally well off, the banking sector is facing the unpleasant future of a credit crunch. The factor that really interests me is how the poorer nations and developing countries’ banking sectors are going to come out of this pandemic.

Debt & Banks

Many of these countries already have large foreign debt and the question that we need to ask objectively is; what can the governments of these countries do in order to help the banks, plus keep the economy alive.

The World Bank, IMF and the West need to take the appropriate actions to help affected countries with loans and not attach strings to the lent money, in order to stabilize the financial sector and economy to stave off hyperinflation.

This is extremely important because the last thing we want to see on the horizon in the next 6-12 months, due to stringent conditions placed on poor countries who take out loans, is a wave of sovereign bankruptcies which could otherwise have been avoided.

Pandemic’s real impact

As countries around the world are trying to come to terms with the pandemic and grapple with infection rates, we are witnessing the fastest levels of job losses since the great depression.

Analysts are forecasting that despite trillions of dollars being pumped into the global economy, more than 15 million jobs will be lost and cause unemployment numbers to spike to unprecedented highs.

The hardest-hit sectors from the pandemic are the Airlines, Tourism, Travel and Entertainment and the Hotel industry. The number of casual workers employed in these industries is extremely high. In the U.S. alone the pandemic could result in the loss of 14 million jobs and that the economy would contract by more than 15%. However, governments in countries like the US and Australia are doing what they can to help their constituents out of a need to ensure re-election.

Overseas

What about Countries like India, Sri Lanka, Pakistan and other low-income countries? More than 1.6 billion people stand to lose their jobs and half that number have already lost jobs due to stringent lockdown measures put in place.

According to the International Labour Organisation (ILO), 81% of the global workforce live in countries with mandatory or recommended closures out of which 37.5% are employed in sectors that have experienced large disruption. ILO also made a prediction that there would be close to 25 million job losses by the end of this year globally.

Will history repeat itself?

It’s grossly inaccurate when many analysts compare the current crisis to past crises. It’s difficult to predict an outcome. The GDP is contracting at an unprecedented rate and employment globally is being buffeted by the economic shocks caused by the lockdowns. The effects of this shock are immediate, large, and fast.

The ILO also made a very critical observation. It is not enough to look at the employment numbers as these figures can be misrepresented. Of those who are still employed, ILO stated that a lot of the workers who are still working have had their working hours cut short dramatically, are on unpaid leave or temporarily stood down, technically employed.

Even though we are entering unprecedented times and no one can predict the future, I can safely say, as a society, we are not going to be floored by this pandemic in the long run. This is a once in a generation cataclysmic event our generations have to endure gracefully.

Everything with force in nature has an opposite force and reaction and with this contraction of the global GDP, there will be a time when we return to business as usual and see the GDP grow beyond previous levels.

In this article we talk about 2 debt traps a lot of people will fall into this year and what to be aware of in order to stay away from them. This article is dedicated to everyone who has decided to look at their financial health and make a conscious step to change their situation.

The years 1970, 1980, 1990, 2000, 2010 and 2020 are decades that have one thing in common. They bore witness to the international market and economy going through extremely difficult times. The good news, we always came out of it stronger, however, these things will continue to happen due to the market always correcting itself in order to bring in to check bad practices.

The best thing about turbulent times is the levelling of the playing field. This is where sense and long term strategy beat market hysteria and fear.

All the volatility in the market presents excellent opportunities to invest in companies with excellent track records of success.

Turbulent times provide anyone with a once in a lifetime opportunity to put aside as much money as they can to build their future wealth.

The way to do this is to first understand what debt traps to avoid so that you have more money to invest instead of being stuck with bad debts that drains your bank balance and leaves you living pay-check to pay-check.

If at all possible, here are the 2 debt traps you should avoid this year:

In this article, we are going to critically analyse the financial and banking industry to see if it has what it takes to avoid a financial meltdown due to the COVID Pandemic.

A little over a decade the globe experienced a financial crisis. Over the last few months, the level of unemployment across the globe dwarfs unemployment during that entire global financial crisis. These unemployment numbers are only going to increase.

Lockdown

More than 2 billion people in the world have gone into a self-imposed or government-mandated lockdown. At the time of writing this article, the world population clock states the globe’s population at 7.8 billion.

55% of the world’s population is urban and 85% of the world’s job market can be found in urban centres.

This effectively means half of the world’s urban force are in essence unemployed (barring a percentage that can work from home).

The banks print money

As reserve banks around the globe are printing trillions in their respective currencies to make sure that banks are able to maintain the flow of cash. Banks around the world are employing different strategies but the most common seem to be offering consumers loan repayment holidays. Many Bank’s employing this strategy in Europe still haven’t fully recovered from the 2008 North Atlantic Financial crisis, where Central Banks deployed the same printing strategy to prop up liquidity.

America at crossroads

The US is also at a crossroad. The current administration reduced the amount of cash banks need to keep in reserve to cover losses before the pandemic drop kicked the globe in the face. Wall Street Had Cut 68,000 Jobs and received trillions in emergency loans prior to COVID-19 anywhere in the world.

The economic cost of this pandemic for the U.S. alone has cost the taxpayers $22.8 trillion.

Rest of the world

Meanwhile, in Europe, taxpayers were told by their politicians that they would no longer be paying to bail out banks. However, in contrast to what was said, before the pandemic in Dec 2019, Germany bailed out Nord Lb bank for the tune of $4 billion.

Countries around the world are abandoning fiscal policies of running a balanced budget and borrowing vast sums of money to protect businesses and industries.

As the health care systems around the world are being pushed to the limit and people are losing their lives the need for critical resources keeps increasing. This places extreme strain on governments as they face growing demands for cash. As a result, many governments are borrowing unprecedented amounts of money to fight the pandemic.

Here in Australia

According to ASIC in 2018, small businesses make a significant contribution to the Australian economy, making up 20% of GDP and employing about half the workforce. Of the 2.4 million Australian companies registered with ASIC, about 96% are small businesses with fewer than 20 employees.

Small businesses in Australia and around the world are under an unprecedented attack due to the COVID 19. The overheads and fixed costs these businesses need to maintain does not stop and are not able to generate any income.

Therefore, every single day, they operate at a loss. The Australian government has stepped in by allowing businesses to access money as part of the stimulus package. The real question that needs to be answered is “is that enough?”

The common problem

The most common problem facing individuals and business at the moment is access to funding. Reports of a lot of server crashes have been an ongoing issue due to a multitude of businesses and individuals accessing the same government websites at the same time.

This pandemic also has a lot of unforeseen effects on Australian companies that depend on seasonal workers such as the food industry in Australia. This sees a lot of Australians residents and temporary working holiday visa holders crossing state borders for harvest. That is very restricted now in the current climate. Also, the current international climate reduces demand and increases competition.

Many firms and small businesses in Australia and around the world need to be able to reopen in a timely manner before it kills their business.

What the banks aren’t telling us

Even though Australia has very robust banking regulations, the banking sectors around the globe, unfortunately, are not prepared for the fall out from the pandemic. Credit has to be given beyond levels compared to 2008, as banking sectors around the globe are in much better shape than before.

The exposure banks have in regards to loans on their balance sheets needs to be played out. Loans from corporates to corporates and if even one of them default on their short term loans the stress on the banking sector would be immense.

Also, the global fall in GDP and the standstill of economic activity has now gone on for a very long period. So how are the banking sector’s non-performing loans faring? They are accumulating and the banks capital and liquidity reserve are not sufficient to deal with this crisis.

My critics would say that banks around the world have learned from the last financial crisis. However, I would like to point out that when planning for a crisis, we planned for a similar 2008 crisis that originated from the financial sector. No bank’s risk models would have been able to determine or predict the current impact the COVID 19 pandemic has on the global economy would have on their capital reserves. This could lead banks facing solvency issues and major companies asking for a bailout.

Bailouts

One needs to look no further than our flight industry with perennial blue chips Qantas being bailed out and Virgin threatening to enter voluntary administration at the time of writing.

Let’s not forget with the bailouts in 2008, very little of the money provided to the banks and other large firms actually went into the everyday economy. They went into dividends, bonuses and share buybacks. This was a very serious breach of taxpayers trust.

However, with the current bailouts and stimulus being churned out globally, I hope the money goes into the real economy to jump-start the fallen GDP.

Governments worldwide need to focus more on bailing out households. This is because households will have a source of income, which leads to them being able to meet their financial commitments.

Financial commitments in the form of day to day bills, mortgage/rent, credit card or personal loans. By bailing out the household, you’re bailing out the financial system and reverse engineering liquidity being pumped into the market.

fahd

fahd